20 Jul 2022

Insight

London

The pace of change in anti-money laundering regulation has been rapid since the 2020 edition of our survey, and shows little sign of slowing down. The EU has introduced a significant AML reform package which is working its way through the legislative process, the UK recently issued responses to consultations on changes to its AML regime, the US enacted new legislation last year…the list goes on. Some reforms reflect the need for AML regulation to adapt to new challenges (such as crypto-assets), and others are responsive to the identification of weaknesses in current frameworks, and incidents where these have been exploited by criminals.

Against that backdrop, it is perhaps unsurprising that AML – which came second in the 2020 survey of the most significant risk and compliance issues faced by trust companies – has retained its prominence, and ranks second again in our survey responses.

As we observed in the introduction to this year's results, the 2022 survey commenced prior to Russia's invasion of Ukraine. The sanctions response to that invasion has of course had particular impacts in the trusts space, including the EU restrictions on the provision of trust services to certain Russian-connected trusts1, and the complexity for trustees of understanding the implications of the designation of some settlors, protectors and/or beneficiaries as being subject to asset freezes under one or more sanctions regimes. Whilst our survey questions focussed on AML in particular, it is clear that financial crime compliance in general remains a critical area of focus.

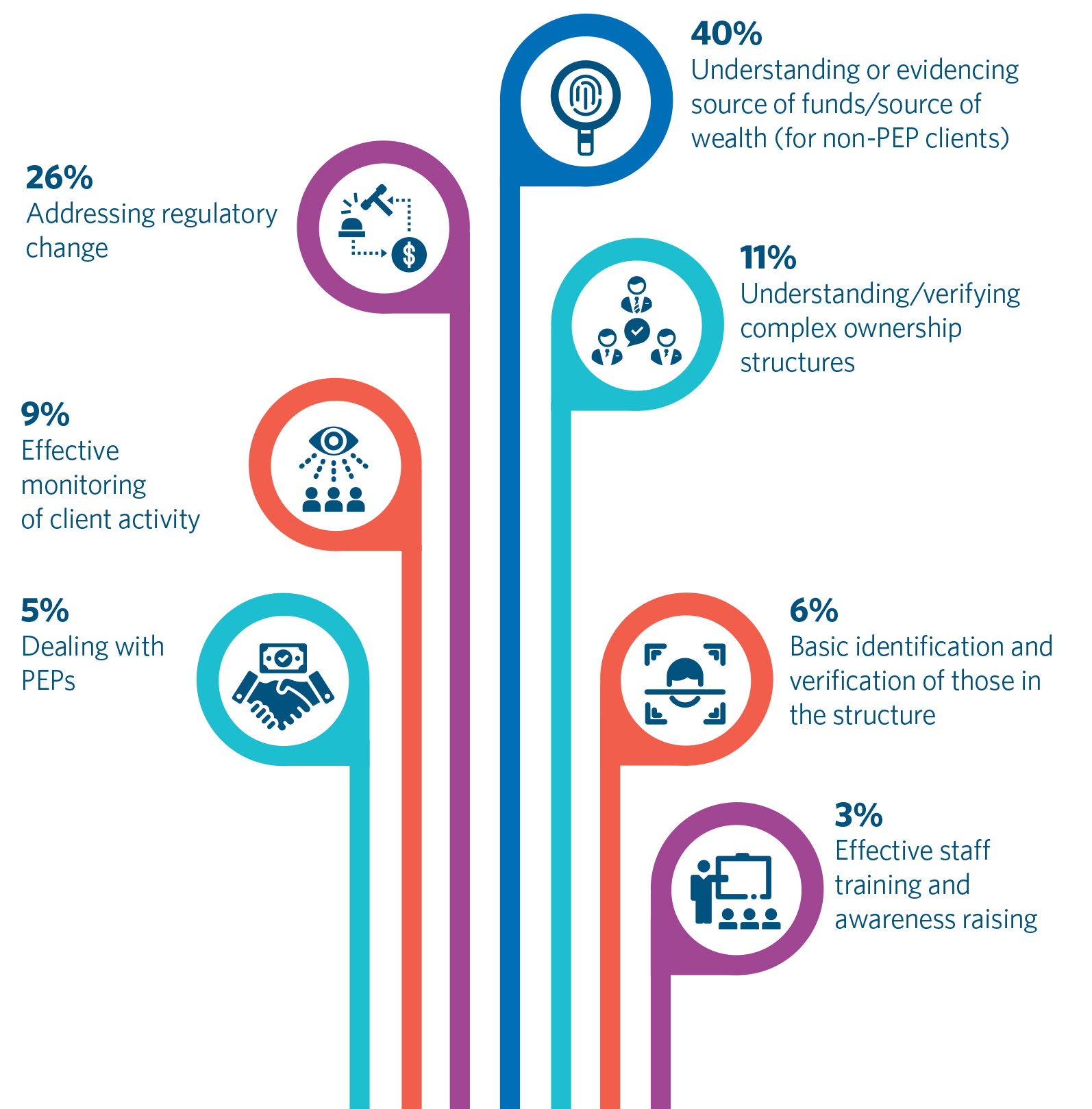

Turning back to AML, we asked in both 2020 and 2022 what the most significant areas of AML challenge were for trustees. The stand-out areas of difficulty in 2022 – by some margin – were understanding or evidencing source of wealth/source of funds for non-PEP clients (40% of responses), and addressing regulatory change (26% of responses).

- Source of wealth/funds was also the most important area of challenge in 2020 (called out by 37% of survey responses), and, as we observed at the time, this is to be expected – obtaining an understanding of the source of funds/wealth of clients is a key means of mitigating the risk of money laundering, but one in which, in many countries, there continues to be limited practical guidance on the verification measures that should be taken.

- Addressing regulatory change was a new category we added in 2022, so there is no direct comparator for 2020, but given the volume of recent and proposed AML regulatory reform, referred to above, it is also unsurprising that this was a key issue for respondents.

Perhaps more interesting is a marked decline in respondents identifying effective monitoring (26% in 2020 to 9% in 2022), understanding and verifying complex ownership structures (24% in 2020 to 11% in 2022, and effective staff training and awareness (18% in 2020 to 3% in 2022) as key areas of challenge. Concerns regarding basic identification and verification, and dealing with PEPs, remained relatively stable (8% each in 2020 and 6% and 5% respectively in 2022). This may be reflective of firms having enhanced their procedures and expertise so as to feel more comfortable with their core AML compliance.

What is the most significant AML compliance challenge for trustees?

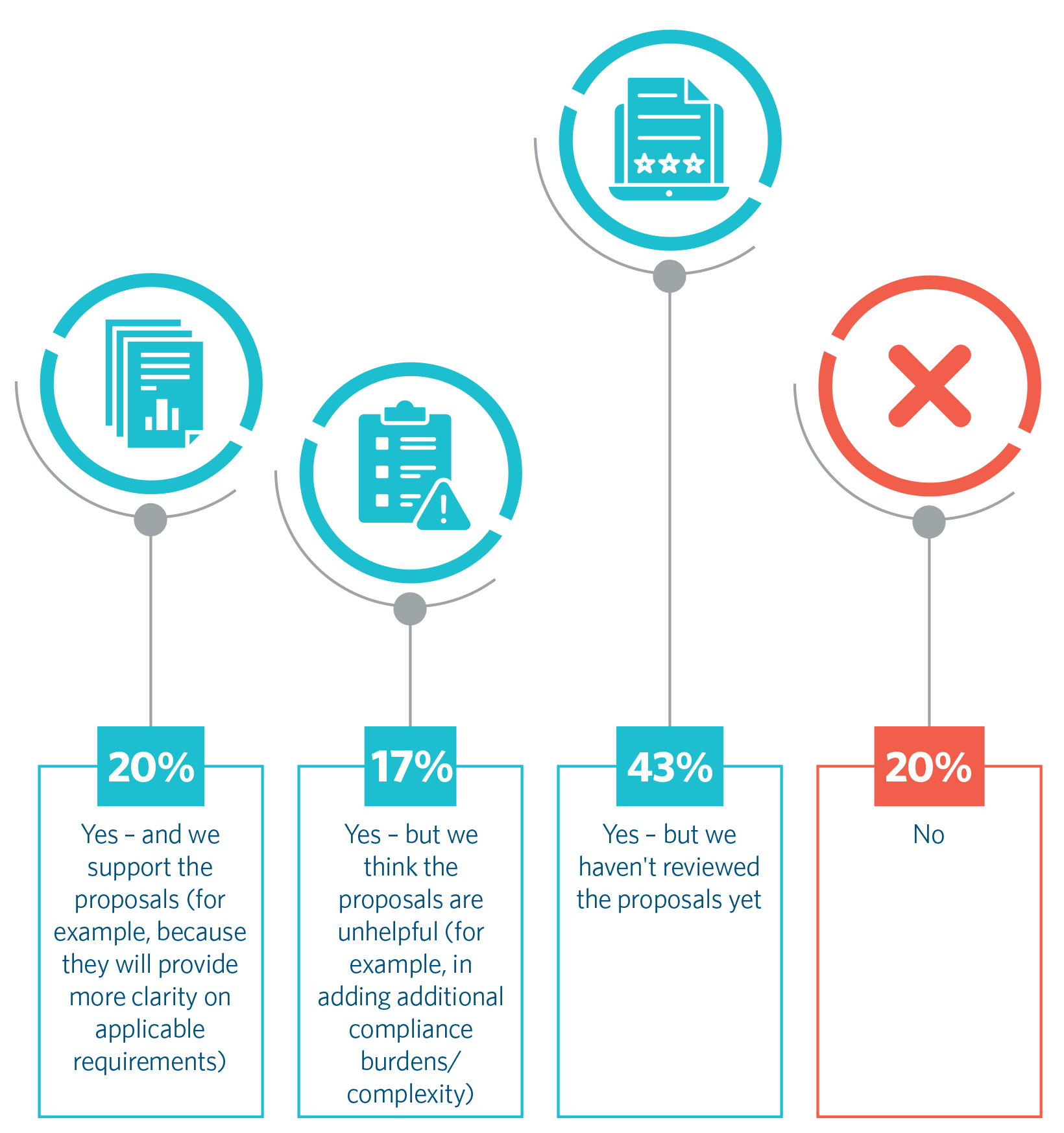

Continuing the theme of regulatory reform, we also asked respondents this year if they would be impacted by the EU AML reform package. A majority (80%) said that they would be, albeit most of these most firms (43% of total respondents) have not yet reviewed the proposals. Given that there are several hundred pages of new regulation which are still changing in response to the trilogue process, this is entirely understandable! For those who want to get a sense of the proposals without reading them, an introduction to the legislative package (as introduced in 2021) can be found here and a deeper dive on the customer due diligence and beneficial ownership provisions (as introduced) here. That said, the proposals continue to develop – one headline point was the European Parliament's proposal in March 20222 that the beneficial ownership threshold for corporate entities3 should be reduced from 25% to 5% at every level of ownership - although it is to be hoped that this gold-plating of the FATF recommendations is not taken forward.

Of those who anticipated that the reforms would impact them and offered a view on the proposals, respondents were almost equally split between those who supported them (20%) and those who thought the reforms were unhelpful (17%).

Significant AML reforms have been proposed in the EU, including moving parts of the Money Laundering Directive into a Regulation, and enhancing the Directive. Will you be impacted by the EU proposals?

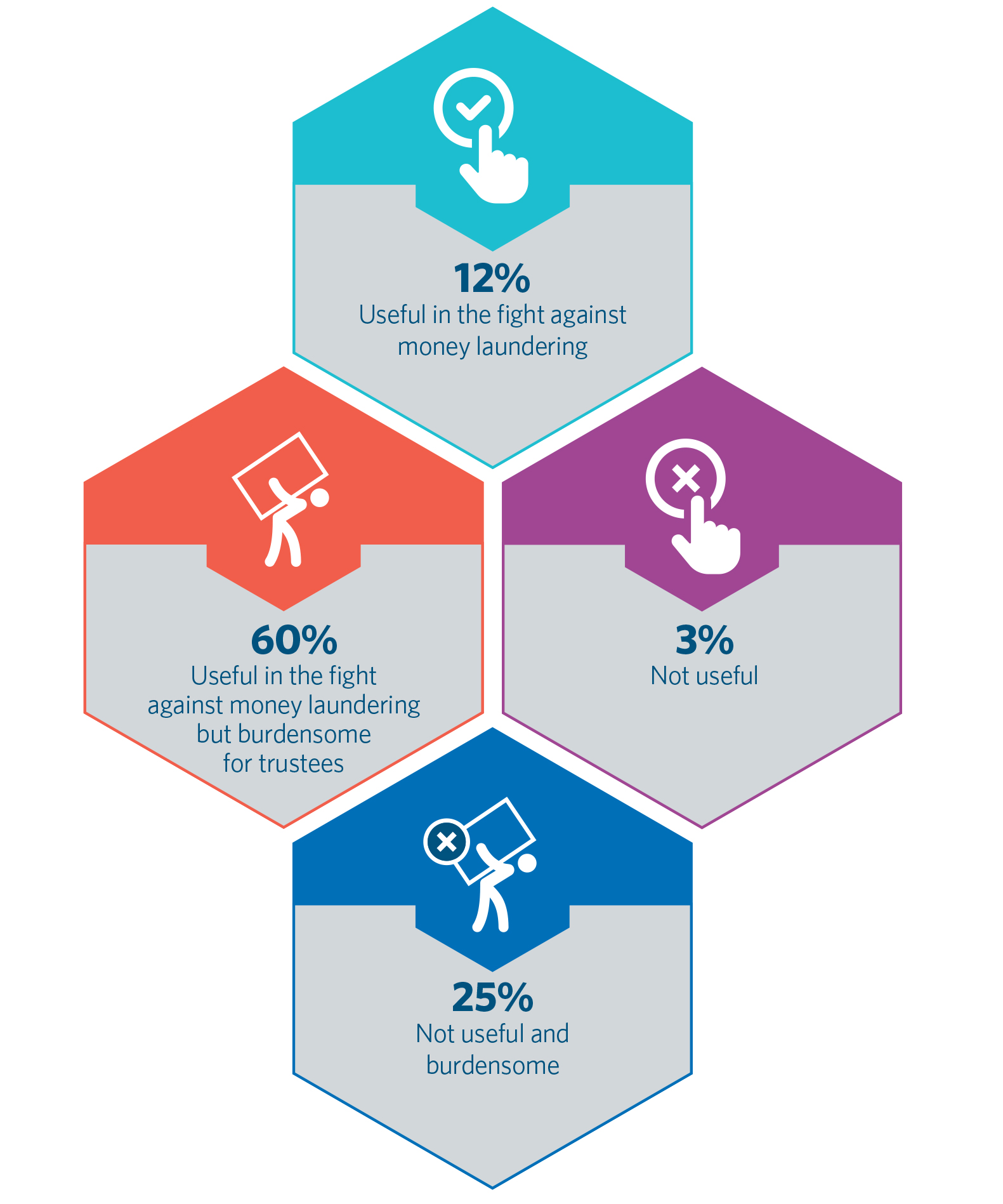

We also drilled down on the question of beneficial ownership registers, which has been an area of some controversy in recent regulatory reform. This was a question we also asked in 2020, and interestingly it seems that views have shifted to some extent. In 2020, a small majority (51%) of respondents thought that these changes were useful, with 14% opting for 'useful' and 27% 'useful but burdensome for trustees'. In 2022, the equivalent figures were 12% and 60% - so a total of 72% had a positive view of such measures, albeit recognising the compliance impact.

The complexity and impact of these measures as they pertain to trusts tends to vary between civil and common law jurisdictions. In the UK, where of course trusts are widely used in a variety of contexts, the introduction of the expanded scope of the Trusts Registration Service (TRS) was recently pushed back to 1 September 20224, amongst other things in light of the IT development work necessary for the TRS to accept registrations from additional types of trusts. Broadly speaking, non-taxable trusts in existence on or after 6 October 2020 must now (unless they are exempt) be registered by 1 September 2022, non-taxable trusts created after September 2022 must be registered within 90 days, and taxable relevant trusts set up on or after 4 June 2022 must be registered within 90 days of the trustees becoming liable to pay UK taxes. Changes to the trust details or circumstances must be registered within 90 days of the change.

Do you think the introduction/enhancement of requirements on trustees relating to reporting information to beneficial ownership registers (for example, the requirements that will be implemented in the EU under 5MLD) will be:

AML business impacts

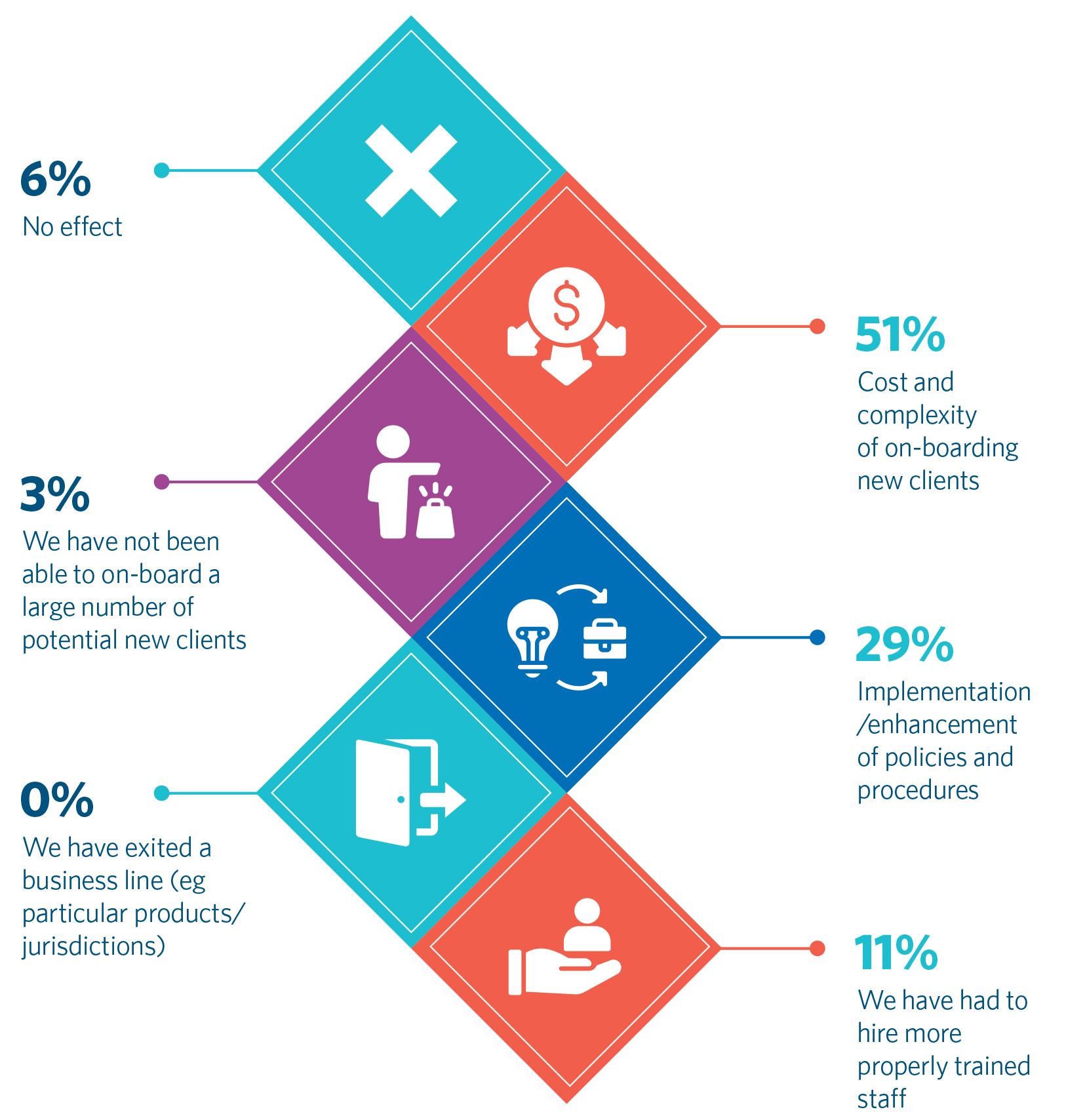

In both 2020 and 2022 we asked survey respondents about the way in which AML compliance has affected their businesses during the year. The responses have not changed significantly over the last two years: the cost and complexity of onboarding new clients remains the key business impact (59% in 2020, and 51% in 2022). The implementation/enhancement of policies and procedures being the second most popular response (not surveyed in 2020, 29% in 2022).

The need to hire more staff with AML experience remained a common but less popular response (27% in 2020 and 11% in 2022), with a small number of firms identifying no business impact at all (10% in 2020, 6% in 2022), and very few firms reporting that they have not been able to onboard a large number of potential new clients (0% in 2020, 3% in 2022), or that they have had to exit a business line (4% in 2020, 0% in 2022).

How has AML compliance most aected your business over the past 12 months?

AML 'exposés'

Finally, we asked respondents about 'leaks' such as the Pandora or Paradise Papers, which have given rise to additional media scrutiny of offshore wealth. There have been a number of leaks of this type over the last few years, and it is a trend which seems likely to continue.

The majority of respondents (60%) considered that leaks of this sort lead to an unfair characterisation of legitimate service providers. Equally, 31% of respondents saw some positives, in that they can focus attention on the need for AML compliance, and identify some improper activity, and 6% – perhaps a surprisingly small number – had used the leaked information in onboarding, retention or SAR activity. Just 3% of respondents saw them as irrelevant to their business.

The 'Pandora papers' are the most recent in a series of 'leaks' which have given rise to additional media scrutiny of oshore wealth. Which of the following statements is most true for your organisation regarding these sorts of leaks:

Whilst the impression of offshore wealth management left by leaks of this sort may be misleading, there is no doubt that it has informed some of the current regulatory scrutiny and impetus for reform. It is to be hoped that – contrary to the expectations of many of our respondents – those reforms bear fruit in making trust and wealth management services more difficult for criminals to access, without placing a disproportionate compliance burden on regulated firms.

- Article 5m of Regulation 833/2014, which relates to trust or similar legal arrangement having as a trustor or a beneficiary: (a) Russian nationals or natural persons residing in Russia; (b) legal persons, entities or bodies established in Russia; (c) legal persons, entities or bodies whose proprietary rights are directly or indirectly owned for more than 50 % by a natural or legal person, entity or body referred to in points (a) or (b); (d) legal persons, entities or bodies controlled by a natural or legal person, entity or body referred to in points (a), (b) or (c); or (e) a natural or legal person, entity or body acting on behalf or at the direction of a natural or legal person, entity or body referred to in points (a), (b), (c) or (d).

- https://www.europarl.europa.eu/doceo/document/CJ12-PR-719945_EN.pdf

- Readers will be aware that the beneficial ownership test for trusts and similar legal arrangements is different.

- https://www.legislation.gov.uk/uksi/2022/137/contents/made

Articles in this series

Key contacts

Legal Notice

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills 2024

Stay in the know

We’ll send you the latest insights and briefings tailored to your needs